There is a profound disconnect between the way geopolitical conflict is discussed in the sterile, soundproofed corridors of political power and the way it is actually felt by a family sitting around a kitchen table in Ohio or London. Over my 17 years in corporate human resources, I sat across from thousands of everyday people – warehouse workers, middle managers, logistics coordinators, and delivery drivers. I learned a universal truth about human behavior: most people do not have the luxury of caring about the ideological posturing of foreign policy. They care about fairness, they care about stability, and they care about whether their paycheck will cover the cost of basic survival at the end of the month.

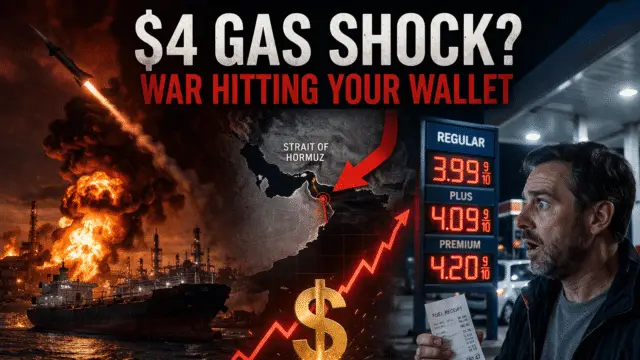

On February 28, 2026, the United States and Israel launched coordinated, targeted military strikes against Iranian military and nuclear infrastructure.1 In the immediate aftermath, the geopolitical commentary class flooded the airwaves, debating military strategy, regional hegemony, and historical grievances. But as an objective social commentator, I look at the world through the lens of cause and effect, stripped of blind tribalism. And the objective reality is this: the moment those strikes occurred, the global supply chain suffered a catastrophic heart attack.

In retaliation, Iranian forces and regional proxies effectively shut down the Strait of Hormuz, the world’s most critical maritime chokepoint.1 What followed was not a distant political event, but an immediate, devastating economic shockwave. Within days, gas prices in the American Midwest surged, European diesel markets panicked, agricultural fertilizers were stranded at sea, and the algorithmic gears of the gig economy began crushing the most vulnerable workers in our cities.

We have spent decades building a hyper-globalized, “just-in-time” economy that prioritizes corporate efficiency over local resilience. We constructed a system so incredibly brittle that a drone strike in the Middle East instantly reaches into your wallet and doubles your cost of living. This report is an unfiltered, exhaustively researched analysis of how the current US-Israel-Iran war is destroying the purchasing power of the working class. It is a story of shipping routes, insurance premiums, agricultural chemistry, and labor exploitation. Most importantly, it is a story about how the structural failures of globalization always, without exception, exact their heaviest toll on the ordinary people who had absolutely nothing to do with the conflict.

The Geography of Vulnerability: Anatomy of a Chokepoint

To understand the sheer magnitude of the economic violence currently rippling across the globe, you must first understand the physical geography of the Strait of Hormuz. It is a narrow waterway, measuring just 33 kilometers at its tightest point, connecting the Persian Gulf to the Gulf of Oman and the Arabian Sea.5 In times of peace, it is the humming, mechanical artery that keeps the modern world functioning. Roughly 100 cargo-carrying vessels traverse it daily, transporting the lifeblood of industrial civilization.6

When the strikes hit on February 28, the retaliatory response was swift. Iranian drone attacks damaged oil and gas facilities, targeted fuel storage terminals, and struck water desalination plants in the Gulf.3 Suddenly, the Strait became a lethal war zone. The collapse of maritime traffic was instantaneous and breathtaking in its severity. A waterway that historically handled an average of 138 vessels per day saw traffic plummet by 90 percent.8 By March 2, total traffic fell to a mere 13 transits, with only a single oil tanker observed risking the journey.9 By March 3, only four ships made the crossing.8

Look at the sheer volume of global energy that relies exclusively on this 33-kilometer stretch of water. Approximately 20 million barrels of oil flow through the Strait of Hormuz every single day.5 That represents roughly 20 percent of total global petroleum liquids consumption, and over 25 percent of all seaborne oil trade.5

| Origin Country | Share of Hormuz Oil & Condensate Exports (Q1 2025 Data) |

| Saudi Arabia | 37.2% |

| Iraq | 22.8% |

| United Arab Emirates | 12.9% |

| Iran | 10.6% |

| Kuwait | 10.1% |

| Qatar | 4.4% |

| Other | 1.9% |

The data above reveals a terrifying concentration of risk.12 Over 93 percent of the crude and condensate moving through this chokepoint originates from just five nations.12 If you want to understand who is hurt most by this, look at the destinations: nearly 90 percent of the crude and condensate traversing the strait is bound for Asian markets, primarily China, India, Japan, and South Korea.6

When the Asian manufacturing sector – the factory of the world – is starved of energy, the cost to produce every conceivable consumer good spikes. Alternative overland routes, such as Saudi Arabia’s East-West Crude Oil Pipeline and the UAE’s Habshan-Fujairah pipeline, boast a combined capacity of only 4.7 million barrels per day.10 When you subtract that from the 20 million barrels normally flowing through the strait, the global market is left staring into the abyss of a 15-million-barrel daily supply shortfall.10

This is the failure of our globalized architecture. The infrastructure required to bypass the Strait of Hormuz simply does not exist. We have allowed the stability of the global economy to rest entirely on a geographic bottleneck located in the most volatile region on Earth. And when that bottleneck snaps shut, the illusion of distance vanishes.

The Maritime Insurance Racket: The Invisible Architects of Inflation

The general public often assumes that shipping halts solely because brave captains refuse to sail their physical vessels into military crossfire. While physical danger is a genuine factor – with at least nine ships damaged since the conflict’s onset – the real paralysis is dictated by actuaries sitting in glass offices in London.13 Modern supply chains do not run on bravery; they run on liability coverage.

As the conflict erupted, the global maritime risk market underwent a structural shock. Major Protection and Indemnity (P&I) insurers issued 72-hour cancellation notices on Gulf war-risk coverage, while reinsurance capacity from London markets was abruptly withdrawn.14 Without reinsurance backing, P&I clubs are legally and financially paralyzed, rendering it functionally impossible for vessels to operate in the designated war zones.14

For the handful of operators willing to play Russian roulette with their multi-million-dollar assets, the cost of specialized war-risk insurance has reached extortionate, usurious levels. Before the conflict began, the hull war-risk premium for a standard tanker valued at $250 million was approximately 0.25 percent, equating to about $625,000 per voyage.15 As of early March 2026, those premiums surged by over 1,000 percent to roughly 3.0 percent.13 That translates to $7.5 million in insurance costs for a single transit.13

Let me be perfectly clear: global shipping conglomerates like Maersk, Hapag-Lloyd, and CMA CGM do not absorb these $7.5 million penalties out of the goodness of their hearts. They pass every single cent down the supply chain. In response to the crisis, these major carriers suspended all Gulf transits and completely abandoned the Suez Canal.8 Instead, they are rerouting their massive fleets entirely around the Cape of Good Hope at the southern tip of Africa.8

This colossal geographical detour adds 10 to 20 days to delivery times.8 It consumes vast quantities of extra bunker fuel, tying up global shipping capacity and instantly generating a severe shortage of available containers. The immediate consequence is a violent explosion in freight rates, tracked rigorously by the Drewry World Container Index.

| Trade Route | Drewry World Container Index Change (March 2026) | Market Reality |

| Global Composite | +3% (reaching $1,958 per 40ft container) | Immediate baseline inflation across all global routes 17 |

| Shanghai to Los Angeles | +10% (reaching $2,402 per 40ft container) | Direct hit to US import costs for manufactured goods 17 |

| Shanghai to New York | +7% (reaching $2,977 per 40ft container) | Increased cost of East Coast deliveries 17 |

| Intra-Asia (IACI) | +18% (reaching $651 per 40ft container) | Asian regional supply chains severely fracturing 18 |

This logistical nightmare extends far beyond retail goods. Consider the construction industry in the United States and the United Kingdom. Nearly a year ago, the industry was already grappling with the inflationary fallout of 25 percent tariffs on imported materials.1 Now, essential materials like cement, steel, concrete, and aluminum – massive quantities of which are produced or sourced in the Middle East – are trapped.1

Contractors facing unpredictable delivery timelines are forced to secure temporary staging to store whatever materials they can find, incurring unplanned expenses for storage, handling, and insurance.1 When a shipment of structural aluminum from Dubai is delayed by a month, construction on an affordable housing project in Ohio grinds to a halt. The labor sits idle, the interest on the construction loan compounds, and the final cost of the home skyrockets. This is how a missile strike in the Persian Gulf directly restricts housing supply and keeps domestic rents artificially high.

The Energy Bloodletting: Bleeding at the Pump

Energy is not merely a sector of the economy; it is the fundamental base reality upon which human civilization operates. Every physical object you touch, every piece of food you consume, and every service you utilize contains the embedded cost of the energy required to extract, manufacture, and transport it. When energy prices surge, the cost of human existence surges in exact proportion.

The immediate aftermath of the February 28 strikes witnessed a violent, historic recalibration of global oil markets. Brent crude, the international benchmark, surged past $92 per barrel on March 6 – a terrifying 28 percent increase in a matter of days.3 As hostilities escalated over the subsequent weekend, with attacks reported on fuel storage terminals in Tehran and Kuwait, outright panic seized the trading floors. In Asian markets, Brent crude spiked to an astonishing $119 per barrel before settling back into the volatile $89 to $100 range.7

For the working-class family in Ohio, this abstract global macroeconomic event translates immediately into visceral, localized financial pain. In early March 2026, the average price of a gallon of gasoline in Ohio jumped by a staggering 65 cents in a single week, reaching $3.43 per gallon.20 In the Cleveland metropolitan area, the average price of regular gasoline spiked from $2.83 to $3.10 almost overnight.21 Across the United States, drivers were paying an average of $3.48 for a gallon of regular gasoline, compared with $2.98 just before the war erupted.22

This sudden erosion of purchasing power operates as a highly regressive tax. It disproportionately punishes hourly wage earners who must commute long distances to manufacturing plants, logistics hubs, or service jobs. An affluent executive can absorb a $15 or $20 increase at the pump without altering their consumption habits; they simply grumble and swipe their credit card. But for a warehouse worker in Akron, Ohio, an extra $80 a month in commuting costs means reallocating capital away from essential groceries, deferring vehicle maintenance, or falling behind on a utility bill.

The situation in Europe is arguably even more precarious due to the continent’s structural reliance on imported diesel. Following the outbreak of the conflict, diesel prices in Europe spiked 27 percent, rising approximately 62 cents per gallon.23 This is a critical metric because commercial transport – the massive trucks that restock grocery store shelves and deliver industrial materials – runs almost exclusively on diesel.10 A 27 percent spike in commercial transit fuel guarantees a secondary, inescapable wave of inflation across all consumer goods.

Political leaders routinely attempt to pacify public anxiety with theatrical announcements regarding Strategic Petroleum Reserves (SPR). We hear promises from the International Energy Agency (IEA) that member states hold over 1.2 billion barrels of public emergency reserves.24 But an objective analysis of the mathematics reveals the profound inadequacy of this safety net. With a daily supply shortfall of roughly 15 million barrels due to the Hormuz blockade 10, even total, unprecedented coordination among global powers can only artificially suppress prices for a matter of weeks. Releasing reserves to combat a systemic chokepoint closure is the economic equivalent of applying a band-aid to a severed artery. It is political theater designed to manage polling numbers, not a structural solution to the working-class energy crisis.

The Fertilizer Shock: Sowing the Seeds of Starvation

One of the most profound, yet chronically underreported, casualties of the Middle East conflict is the global agricultural sector. The average consumer walking down the aisle of a brightly lit supermarket rarely connects a geopolitical skirmish in the Persian Gulf with the price of a loaf of bread or a gallon of milk. Yet, the connection is direct, chemical, and mathematically absolute.

Modern global food security is entirely dependent on synthetic fertilizers, specifically nitrogen-based fertilizers like urea and anhydrous ammonia. The primary feedstock required to produce nitrogen fertilizer is natural gas. The Middle East, blessed with abundant natural gas reserves, has transformed itself into a dominant global force in this sector. Qatar, Saudi Arabia, Bahrain, and Oman are some of the world’s largest fertilizer exporters.26

The statistics are grim: between a quarter and a third of the global trade in the raw materials for fertilizer passes directly through the Strait of Hormuz.27 Furthermore, countries exposed to disruptions in this region account for nearly 49 percent of global urea exports and about 30 percent of global ammonia exports.11

As the shipping blockade took hold in late February and early March 2026, the global agricultural market was plunged into a state of sheer panic. Recognizing the catastrophic implications of stranded supply, fertilizer prices spiked by an alarming 6.5 percent almost immediately.30 By March 9, the North America fertilizer price index topped out at $810 per short ton, eclipsing the previous peak seen in the summer of 2025.32

This disruption could not have occurred at a more disastrous time for American agriculture. The United States, despite having a robust domestic industry, relies heavily on imported fertilizer to meet its massive agricultural demands.33 Approximately 50 percent of the nitrogen used on American corn is applied during the critical spring planting season, which begins in April.32

Corn is a notoriously fertilizer-intensive crop; it demands massive amounts of nitrogen to achieve the yields necessary to keep the agricultural economy afloat. When the cost of nitrogen skyrockets to $810 a ton, and the physical supply is stranded on anchored bulk carriers thousands of miles away, the fundamental economics of American farming collapse.32

I believe in objective cause and effect. Faced with exorbitant input costs and the terrifying prospect that the physical fertilizer may simply not arrive in time, farmers are forced into an impossible corner. Industry analysts and agricultural economists observe that many farmers are rapidly altering their 2026 cropping decisions, shifting millions of acres away from nitrogen-heavy corn and planting soybeans instead, which require significantly less fertilizer.11

While this defensive maneuver may save the individual farmer from immediate financial insolvency, it creates a massive, devastating macroeconomic distortion. A sudden reduction in the domestic corn supply triggers a domino effect across the entire food chain. Corn is the foundational ingredient in livestock feed. When corn yields plummet, the cost to feed cattle, poultry, and swine skyrockets.

Ranchers, unable to afford exorbitant feed prices, are forced to cull their herds prematurely. In the short term, this floods the market with meat, masking the crisis. But in the long term, it severely shrinks the breeding stock. This dynamic guarantees a temporary glut followed by a severe, multi-year catastrophic shortage.34 This is the grim reality of the “input cost trap”.31 The US-Israel-Iran war is effectively locking in a delayed but severe food inflation cycle that will outlast the immediate energy shock and stretch deep into 2027 and beyond.30 You will be paying for the geopolitical failures of 2026 at the grocery checkout counter for the next five years.

The Supermarket Reality: The Erasure of the Working-Class Margin

The cascading, systemic failures in energy markets, maritime shipping, and agricultural inputs ultimately converge at the terminal point of the global economy: the grocery store checkout counter. For a family striving to maintain stability, dignity, and health in a volatile world, the supermarket is where abstract macroeconomic data becomes a brutal, daily reality.

Prior to the outbreak of the war, there was a fragile, desperate optimism that the relentless grocery inflation of the post-pandemic era was finally cooling. The US Department of Agriculture (USDA) had tentatively projected that food-at-home prices would rise by a modest 1.7 to 2.5 percent in 2026, slightly below the 20-year historical average.36 Egg prices, which had caused immense consumer pain previously, were actually predicted to decline.36

However, the Middle East conflict has violently derailed these projections. Food prices and energy prices move in absolute lockstep.10 The cost of diesel dictates the cost of the refrigerated trucks transporting produce across the country. The cost of petroleum dictates the price of the plastic packaging keeping food sanitary on the shelves. The cost of natural gas dictates the fertilizer that grows the crops.10

In the United Kingdom, the impact has materialized with terrifying speed. British grocery price inflation rose to 4.3 percent in the four weeks leading up to late February 2026, abruptly ending four consecutive months of easing food inflation.39 Compare this to the broader UK headline inflation rate of approximately 2.2 percent, and it becomes clear that the cost of mere survival is vastly outpacing general economic metrics.40

The objective data reveals a sobering consumer behavioral shift. The disparity between foodstore sales value and volumes clearly indicates that consumers are paying significantly more money while taking home fewer physical items.42 Retail spend on essential proteins, such as beef, rose 4.6 percent year-over-year, absorbing an increasingly disproportionate share of lower-income household budgets.42 In the US, the USDA noted that beef and veal prices were already 15.0 percent higher in January 2026 than the previous year, driven by that shrinking cattle herd mentioned earlier.34 With the current conflict guaranteeing higher feed costs, the USDA anticipates red meat prices to jump an average of 4.3 percent in 2026, with beef and veal soaring by an astounding 9.4 percent.36

| UK Supermarket Value Ranking (March 2026) | Market Positioning | Impact on Working-Class Consumers |

| Aldi | Cheapest overall | Experiencing massive footfall as consumers aggressively trade down to survive 43 |

| Lidl | Second cheapest | Capturing volume from mid-tier chains; essential staples remain focus 43 |

| Asda | Best-value big supermarket | Maintaining volume through bulk essential-range staples and family baskets 43 |

| Tesco / Morrisons | Mid-market | Relying heavily on loyalty pricing (Clubcard) to retain increasingly desperate shoppers 43 |

This hyper-inflation of essentials is an insidious, regressive tax that disproportionately punishes the working class. An affluent household can absorb a 15 percent increase in the cost of ground beef; they simply allocate less capital to their vacation fund or investment portfolio. But for a household hovering near the poverty line in Ohio or London, there is no discretionary spending left to cut. When the price of basic staples – flour, sugar, milk, and meat – surges, the only mathematical recourse is caloric reduction, skipping meals, or relying on charitable intervention.

The strain on emergency food infrastructure is the clearest indicator of societal failure. During previous periods of acute economic stress and government uncertainty, Ohio’s network of foodbanks saw a staggering 46.2 percent increase in pantry visitors.45 They were forced to distribute millions of additional pounds of food to families who had never previously required assistance.45 The current geopolitical shock, combining surging fuel costs with soaring grocery bills, places these vital community safety nets under immense, unsustainable pressure.46 It is a profound moral failure when a society’s working class, employed and striving, cannot afford the calories necessary to sustain their own labor.

The Gig Economy Trap: The Human Shield of the Supply Chain

To fully comprehend the depth and cruelty of this crisis, we must look beyond the macro-level statistics and examine the micro-level exploitation occurring on the rain-slicked streets of major Western cities. In my 17 years in corporate HR, I have studied labor classification, compensation structures, and the endless pursuit of corporate efficiency. What I see happening today in the gig economy is nothing short of structural violence. The modern economy has brilliantly and ruthlessly shifted the burden of macroeconomic volatility directly onto the shoulders of the most vulnerable labor demographic imaginable.

In London, and across the globe, the final mile of the supply chain relies heavily on an army of on-demand delivery drivers and ride-hailing operators.48 A significant percentage of this workforce consists of migrant laborers.50 Here is where my core philosophy demands nuance and absolute objectivity. Fairness and the rule of law require a strict opposition to illegal migration and entitled behavior that undermines social cohesion or strains local resources. A nation must have borders. But genuine objectivity also demands a fierce, unapologetic defense of the honest migrant who is legally navigating a grueling, exploitative system simply to earn a living and provide for their family. I will not tolerate racism, and I will not tolerate the blind tribalism that scapegoats the worker at the bottom of the pyramid while ignoring the corporate architects at the top.

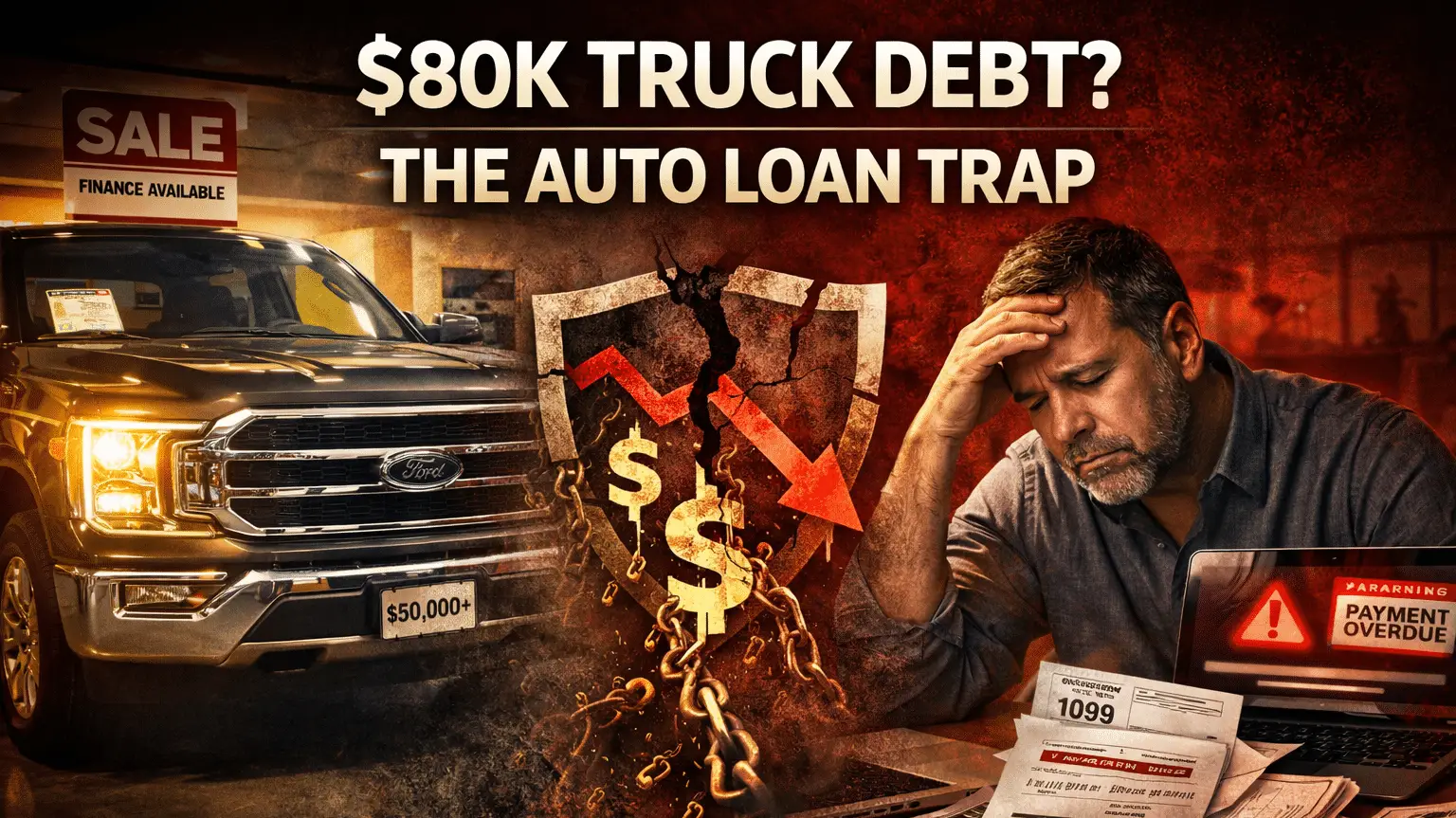

These gig workers are currently trapped in a mathematically impossible scenario. Gig economy platforms operate via algorithmic management, assigning jobs, monitoring performance, and calculating base pay with ruthless efficiency.51 Delivery drivers and couriers operate as self-employed independent contractors. This legal classification is the holy grail for gig corporations, as it means the workers themselves must pay for their own vehicle maintenance, their own insurance, and – most crucially in the context of the Middle East war – their own fuel.52

When the US-Israel strikes on Iran triggered a 27 percent spike in European diesel prices 23, driving fuel costs to £1.51 or £1.60 per litre 53, the algorithms governing these multi-billion-dollar delivery apps did not automatically increase the base payout to compensate for the geopolitical energy shock. Consequently, an honest migrant delivery driver navigating the streets of London is forced to absorb the entirety of a global energy crisis out of their own meager wages.

Research from Cambridge University indicates that a staggering 75 percent of UK delivery and driver gig workers report intense anxiety over potential income drops.52 They suffer physical pain, and they spend an average of ten hours a week logged onto applications waiting for work without earning a single penny.52 When the cost of fuel surges, the net hourly wage of a gig worker plummets, often falling drastically below the legal minimum wage.51

This dynamic reveals the profound hypocrisy of the modern socio-economic structure. Corporate platforms proudly highlight their efficiency and technological innovation to shareholders. Yet, that efficiency is entirely subsidized by offloading the geopolitical risk of energy markets onto marginalized individuals.50 The honest worker is squeezed by opaque algorithms from above and $100-a-barrel oil from below, left to act as a human shock absorber for a war they have absolutely no stake in.

This is the point where the struggles of the native working class and the honest migrant intersect. Both are being crushed by the same corporate indifference and global supply chain fragility. The factory worker in Ohio paying $3.43 a gallon to commute to a manufacturing job 20 and the delivery driver in London paying £1.60 a litre to deliver a meal 53 are victims of the exact same systemic failure. Pitting them against each other is a distraction from the structural rot of an economy that places all risk on labor and all reward on capital.

The Macroeconomic Reckoning: Inflation and the Illusion of Prosperity

The cumulative effect of energy spikes, shipping paralysis, agricultural shortages, and labor exploitation ultimately aggregates into national macroeconomic data. And the warning signs currently flashing across the desks of central bankers are severe, pointing directly toward a prolonged period of economic misery: the dreaded specter of stagflation – stagnant growth coupled with high inflation.

In the United Kingdom, the Office for Budget Responsibility (OBR) delivered a stark, unforgiving assessment of the crisis. Prior to the war, there was a tentative expectation that inflation would continue its slow, painful downward trajectory toward the official 2 percent target. However, the OBR has explicitly warned that the energy price shock triggered by the Middle East crisis could push UK inflation back up to 3 percent by the end of 2026 – a full percentage point higher than previously forecast.19 David Miles, a senior figure at the OBR, stated unequivocally that if these energy prices are sustained, it will deliver a “material, significant,” “noticeable,” and “unwelcome” increase in living costs for British households.19

The destruction of household wealth is mathematically precise and deeply tragic. According to the Resolution Foundation, living standards for typical working-age households in the UK were on track to grow by a modest £300 (0.9 percent) over the coming year.54 For lower-income households, an £800 bump was anticipated due to adjustments in universal credit and the lifting of the two-child benefit cap.54

However, the brutal reality of the global supply chain has obliterated these gains before they could even be felt. The energy price shock alone is projected to add roughly £500 to typical annual household energy bills.54

| UK Household Demographic | Expected 2026 Living Standard Gain (Pre-War) | Conflict Energy Bill Penalty | Net Impact on Household Financial Reality |

| Typical Working-Age | +£300 | -£500 | -£200 (Net Loss, Erasing All Economic Progress) 54 |

| Lower-Income | +£800 | -£500 | +£300 (Gains Severely Eroded, Vulnerability Remains High) 54 |

In the United States, the macroeconomic indicators are equally concerning. The Institute for Supply Management’s Purchasing Managers’ Index (PMI) indicated that prices across the manufacturing sector surged to their highest levels since June 2022, driven by a toxic combination of new tariffs and the sudden explosion in oil costs.56 Furthermore, nearly 30 percent of Ohio manufacturers cited political uncertainty as heavily hampering growth – the highest level recorded since tracking began in 2018.57

The dilemma for central banks like the Federal Reserve and the Bank of England is profound and inescapable. Conventional monetary policy dictates that you combat inflation by raising interest rates to cool consumer demand. However, the inflation currently ravaging the economy is not demand-driven; consumers are not wildly overspending on luxury goods. It is supply-driven.

Raising interest rates will not reopen the Strait of Hormuz. It will not manufacture synthetic nitrogen fertilizer out of thin air. It will not reduce the maritime insurance premiums set by underwriters in London, nor will it magically teleport stranded aluminum to an Ohio construction site. Raising interest rates will only further punish the working-class family attempting to secure a mortgage, or the small business trying to finance operations, compounding the economic pain without solving the underlying supply deficit.53 We are using a sledgehammer to fix a plumbing leak, and the working class is standing directly in the swing path.

Conclusions: The Inescapable Reality of Objective Economics

The current state of the global economy serves as a brutal, undeniable indictment of modern globalization’s inherent fragility. Over the past several decades, the relentless pursuit of absolute corporate efficiency birthed a tightly woven, hyper-optimized supply chain that prioritized immediate cost reduction over long-term resilience.59 By concentrating the flow of the world’s most critical commodities – oil, natural gas, and fertilizer – through vulnerable, narrow geographic apertures like the Strait of Hormuz, the architects of the global economy created a system exquisitely susceptible to catastrophic, instantaneous failure.

The US-Israel-Iran conflict of early 2026 has proven, yet again, that political rhetoric and tribalistic allegiances offer absolutely no shelter from the unforgiving laws of supply and demand. A $100 barrel of oil does not possess a political affiliation, nor does it care about the ideological justifications for military action. It simply exists as a heavy, mathematical weight, pressing down indiscriminately on the budgets of working-class families across the globe.

When the cost of living doubles due to supply chain paralysis, it is the factory worker in Ohio and the honest migrant delivery driver in London who pay the ultimate, devastating price. They are the ones who must navigate the reality of $3.43 per gallon gasoline, the 4.3 percent surge in grocery inflation, the $810 per ton fertilizer spikes, and the total erasure of any meaningful growth in their living standards.

To address these profound vulnerabilities, objective realism must replace political theater. We can no longer afford to be governed by corporate buzzwords or naive globalist assumptions. Nations must radically reassess their dependence on distant, unstable chokepoints for the energy and agricultural inputs that sustain their populations. True sovereignty is not merely a matter of military might or border security; it is the fundamental capacity to feed, fuel, and house a population without relying on the safe passage of a cargo ship through a war zone thousands of miles away.

We must rebuild local industrial capacity, secure resilient domestic energy and agricultural supply chains, and foster a labor market that rewards honest work rather than exploiting algorithmic loopholes. Until the structural flaws of global supply chains are acknowledged and rectified with unapologetic objectivity, the working class will continue to serve as the involuntary human shock absorbers for every geopolitical crisis that ignites across the globe. Fairness demands a better system. The rule of law demands a better system. And human dignity requires it.

Works cited

- The 2026 Iran War and Its Global Impact on Construction Supply Chains | Baker Donelson, accessed on March 11, 2026, https://www.bakerdonelson.com/the-2026-iran-war-and-its-global-impact-on-construction-supply-chains

- Middle East Conflict: Implications for Energy, Inflation, and CRE – Cushman & Wakefield, accessed on March 11, 2026, https://www.cushmanwakefield.com/en/insights/middle-east-conflict

- What Does the Iran War Mean for Global Energy Markets? – CSIS, accessed on March 11, 2026, https://www.csis.org/analysis/what-does-iran-war-mean-global-energy-markets

- Iran has largely halted oil and gas exports through strait of Hormuz – The Guardian, accessed on March 11, 2026, https://www.theguardian.com/world/2026/mar/03/iran-has-largely-halted-oil-and-gas-exports-through-strait-of-hormuz

- Hormuz: the world’s energy fuse – Middle East Monitor, accessed on March 11, 2026, https://www.middleeastmonitor.com/20260309-hormuz-the-worlds-energy-fuse/

- Charted: Global Energy Flows at Risk in the Strait of Hormuz – Visual Capitalist, accessed on March 11, 2026, https://www.visualcapitalist.com/chart-energy-flows-at-risk-strait-of-hormuz/

- The Iran Conflict Is Sending Oil Prices Soaring – What Happens Next?, accessed on March 11, 2026, https://www.csis.org/analysis/iran-conflict-sending-oil-prices-soaring-what-happens-next

- Global trade reroutes to Cape of Good Hope while traffic in Strait of Hormuz plunges 90%, accessed on March 11, 2026, https://www.aa.com.tr/en/live/global-trade-reroutes-to-cape-of-good-hope-while-traffic-in-strait-of-hormuz-plunges-90-/3851150

- No One, Not Even Beijing, Is Getting Through the Strait of Hormuz – CSIS, accessed on March 11, 2026, https://www.csis.org/analysis/no-one-not-even-beijing-getting-through-strait-hormuz

- How will soaring oil prices caused by Iran war impact food costs …, accessed on March 11, 2026, https://www.aljazeera.com/news/2026/3/10/how-will-soaring-oil-prices-caused-by-iran-war-impact-food-prices

- Middle East Tensions Raise Spring Planting Concerns | Market Intel, accessed on March 11, 2026, https://www.fb.org/market-intel/middle-east-tensions-raise-spring-planting-concerns

- Charted: Oil Trade Through the Strait of Hormuz by Country – Visual Capitalist, accessed on March 11, 2026, https://www.visualcapitalist.com/charted-oil-trade-through-the-strait-of-hormuz-by-country/

- How Maritime Insurance Rates Reflect a Widening Middle East War, accessed on March 11, 2026, https://moderndiplomacy.eu/2026/03/06/how-maritime-insurance-rates-reflect-a-widening-middle-east-war/

- March 8, 2026: Iran War Maritime Intelligence Daily, accessed on March 11, 2026, https://windward.ai/blog/march-8-maritime-intelligence-daily/

- Maritime Premiums Surge As U.S-Iran War Widens To The Mediterranean Region, accessed on March 11, 2026, https://www.marineinsight.com/shipping-news/maritime-premiums-surge-as-us-iran-war-widens-to-mediterranean-region/

- 2026 Strait of Hormuz crisis – Wikipedia, accessed on March 11, 2026, https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis

- Service Expertise – World Container Index – 05 Mar – Drewry, accessed on March 11, 2026, https://www.drewry.co.uk/supply-chain-advisors/supply-chain-expertise/world-container-index-assessed-by-drewry

- Latest Trackers and Indices – Drewry Maritime Research, accessed on March 11, 2026, https://www.drewry.co.uk/trackers-and-indices/latest-trackers-and-indices

- Middle East crisis could push UK inflation back up to 3%, warns …, accessed on March 11, 2026, https://www.theguardian.com/business/2026/mar/10/uk-inflation-could-rise-1-because-of-middle-east-crisis-says-obr

- Ohio’s average gas price jumped 65 cents in a week. Experts blame …, accessed on March 11, 2026, https://www.wosu.org/2026-03-09/ohios-average-gas-price-jumped-65-cents-in-a-week-experts-blame-the-iran-war

- Gas Prices Spike in Greater Cleveland and Ohio After Iran Attack – National Today, accessed on March 11, 2026, https://nationaltoday.com/us/oh/cleveland/news/2026/03/04/gas-prices-spike-in-greater-cleveland-and-ohio-after-iran-attack/

- How the Iran war and surging oil prices are affecting consumers at the gas pump and beyond, accessed on March 11, 2026, https://apnews.com/article/iran-war-oil-prices-gasoline-economy-consumers-a5b47c09f83406adf2a00616382003f6

- Gasoline and diesel prices spike overnight as anxious drivers fill up tanks, accessed on March 11, 2026, https://apnews.com/article/iran-oil-gas-gallon-aaa-e2daee318b8e3e6a1124713909a410e4

- UK, Germany and Italy ‘working together’ to navigate commercial shipping through strait of Hormuz – as it happened, accessed on March 11, 2026, https://www.theguardian.com/business/live/2026/mar/10/oil-price-drops-stocks-rebound-trump-iran-war-end-market-news

- Nations worldwide move to conserve fuel as Strait of Hormuz closure threatens global economy – The Cradle, accessed on March 11, 2026, https://thecradle.co/articles/nations-worldwide-move-to-conserve-fuel-as-strait-of-hormuz-closure-threatens-global-economy

- The Iran war: Potential food security impacts – IFPRI, accessed on March 11, 2026, https://www.ifpri.org/blog/the-iran-war-potential-food-security-impacts/

- ‘A big burden for farmers’: Gulf shipping crisis threatens food price shock, accessed on March 11, 2026, https://www.theguardian.com/business/2026/mar/05/big-burden-for-farmers-gulf-shipping-crisis-threatens-food-price-shock

- All Eight Major Fertilizers See Prices Move Higher Compared to Last Month, accessed on March 11, 2026, https://www.dtnpf.com/agriculture/web/ag/crops/article/2026/02/18/eight-major-fertilizers-see-prices

- Middle East tensions raise the stakes in acreage debate, accessed on March 11, 2026, https://www.michiganfarmnews.com/middle-east-tensions-raise-the-stakes-in-acreage-debate

- Geopolitical Firestorm: Fertilizer Prices Surge 6.5% as “Operation Epic Fury” Paralyzes Global Supply Chains, accessed on March 11, 2026, https://markets.financialcontent.com/stocks/article/marketminute-2026-3-4-geopolitical-firestorm-fertilizer-prices-surge-65-as-operation-epic-fury-paralyzes-global-supply-chains

- Fertilizer Shock: 6.5% Price Surge Threatens Global Food Security Amidst Commodity Cooling – Markets, accessed on March 11, 2026, http://business.times-online.com/times-online/article/marketminute-2026-3-10-fertilizer-shock-65-price-surge-threatens-global-food-security-amidst-commodity-cooling

- Iran conflict cripples global fertilizer supply, accessed on March 11, 2026, https://www.farmprogress.com/farm-policy/iran-conflict-cripples-global-fertilizer-supply

- Prolonged Iran War Could Shrink US Corn Acres, Analysts Say, accessed on March 11, 2026, https://farmpolicynews.illinois.edu/2026/03/prolonged-iran-war-could-shrink-us-corn-acres-analysts-say/

- Food Price Outlook – Summary Findings | Economic Research Service – ers.usda.gov, accessed on March 11, 2026, https://www.ers.usda.gov/data-products/food-price-outlook/summary-findings

- Forget oil and gas, a bigger Iran war risk is shaping up, accessed on March 11, 2026, https://m.economictimes.com/news/economy/foreign-trade/forget-oil-and-gas-a-bigger-iran-war-risk-is-shaping-up/articleshow/129207761.cms

- Grocery Prices Are Finally Expected to Cool This Year. Just Not for These Staples, accessed on March 11, 2026, https://money.com/grocery-prices-2026-outlook/

- Grocery prices are set to rise in 2026, accessed on March 11, 2026, https://www.grocerydive.com/news/food-at-home-prices-increase-2026-usda/813359/

- Strait of Hormuz disruptions: Implications for global trade and development |, accessed on March 11, 2026, https://unctad.org/publication/strait-hormuz-disruptions-implications-global-trade-and-development

- Surprise jump in UK grocery inflation makes interest rate cut less probable – The Guardian, accessed on March 11, 2026, https://www.theguardian.com/business/2026/mar/03/uk-grocery-inflation-middle-east-war-eurozone-uk-ecb-worldpanel

- UK Grocery Inflation Climbs to 4.3 Percent Amid Supply Pressures – Doing Business in Bentonville, accessed on March 11, 2026, https://www.dbbnwa.com/articles/uk-grocery-inflation-climbs-to-4-3-percent-amid-supply-pressures/

- UK grocery inflation rises as seasonal spending jumps – Invezz, accessed on March 11, 2026, https://invezz.com/news/2026/03/03/uk-grocery-inflation-rises-as-seasonal-spending-jumps/

- Spotlight: UK Grocery Report – 2025 – Savills, accessed on March 11, 2026, https://www.savills.co.uk/research_articles/229130/379213-0

- We Compared Aldi, Tesco, Asda, Morrisons, Sainsbury’s and Ocado – Here’s the Cheapest Weekly Shop in Britain. – MoneyMagpie, accessed on March 11, 2026, https://www.moneymagpie.com/save-money/cheapest-supermarket-in-the-uk-study-reveals-the-most-budget-friendly-options

- This supermarket is cheaper to shop at than Lidl, exclusive data reveals | The Independent, accessed on March 11, 2026, https://www.the-independent.com/extras/indybest/food-drink/cheapest-supermarket-uk-2026-b2931731.html

- Federal Government Shutdown – Ohio Association of Foodbanks, accessed on March 11, 2026, https://ohiofoodbanks.org/federal-government-shutdown/

- WFP warns rising food and fuel prices risk pushing global hunger higher as humanitarian needs grow, accessed on March 11, 2026, https://www.wfp.org/news/wfp-warns-rising-food-and-fuel-prices-risk-pushing-global-hunger-higher-humanitarian-needs

- WFP Warns Rising Food and Fuel Prices Risk Pushing Global Hunger Higher as Humanitarian Needs Grow, accessed on March 11, 2026, https://wfpusa.org/news/rising-food-and-fuel-prices-risk-pushing-global-hunger-higher/

- Will 2026 be the year that the gig economy booms on shop floors? – Retail Gazette, accessed on March 11, 2026, https://www.retailgazette.co.uk/blog/2026/03/2026-year-gig-economy/

- Why gig workers are protesting around the world – What in the World podcast, BBC World Service – YouTube, accessed on March 11, 2026, https://www.youtube.com/watch?v=8Hnr9n7J4xA

- Full article: Embodied Precariat and Digital Control in the “Gig Economy”: The Mobile Labor of Food Delivery Workers – Taylor & Francis, accessed on March 11, 2026, https://www.tandfonline.com/doi/full/10.1080/10630732.2021.2001714

- The Gig Trap: Algorithmic, Wage and Labor Exploitation in Platform Work in the US | HRW, accessed on March 11, 2026, https://www.hrw.org/report/2025/05/12/the-gig-trap/algorithmic-wage-and-labor-exploitation-in-platform-work-in-the-us

- Riders and drivers in the UK gig economy suffer anxiety over ratings and pay, accessed on March 11, 2026, https://www.cam.ac.uk/stories/gig-economy-anxiety-ratings-pay

- How will war in the Middle East affect your finances? | UK cost of living crisis | The Guardian, accessed on March 11, 2026, https://www.theguardian.com/business/2026/mar/04/iran-war-middle-east-affect-finances-energy-bills-inflation-interest-rates

- War in Middle East ‘could wipe out growth in UK living standards …, accessed on March 11, 2026, https://www.theguardian.com/business/2026/mar/04/war-in-middle-east-could-wipe-out-growth-in-uk-living-standards

- Growth in living standards threatened by war in Middle East – Article Ashington : Walsh & Co, accessed on March 11, 2026, https://www.ashingtonaccountant.co.uk/news/business-news/archive/article/2026/March/growth-in-living-standards-threatened-by-war-in-middle-east

- Prices surge to highest level since 2022 as Middle East conflict escalates: PMI, accessed on March 11, 2026, https://www.supplychaindive.com/news/pmi-february-prices-surge-highest-level-since-2022-middle-east-conflict/813523/

- Ohio manufacturers split on tariff impact – Signal Cleveland, accessed on March 11, 2026, https://signalcleveland.org/tariffs-impact-on-ohio-manufacturers-mixed-why-some-benefit-and-others-lose/

- How high could oil prices go – and what might the global economic fallout be?, accessed on March 11, 2026, https://www.theguardian.com/business/2026/mar/09/how-high-could-oil-go-and-what-might-the-global-economic-fallout-be

- Globalisation is under threat from Iran war – and Britain is uniquely vulnerable, accessed on March 11, 2026, https://www.theguardian.com/world/2026/mar/05/globalisation-under-threat-britain-economy-iran-conflict

Leave a Reply