Introduction: The Anatomy of a Modern Global Energy Crisis

The global economy is currently navigating a severe and unprecedented supply-side disruption following the outbreak of an intense military conflict between the United States, Israel, and Iran in late February 2026. The rapid escalation of these hostilities has fundamentally altered the geopolitical landscape of the Middle East, culminating in the functional closure of the Strait of Hormuz to Western commercial shipping. As the primary maritime artery connecting the oil-rich Persian Gulf to international markets, the Strait accommodates approximately twenty percent of the world’s daily crude oil supply—roughly twenty million barrels per day—alongside significant volumes of liquefied natural gas (LNG), refined petroleum products, and petrochemical fertilizers.1

The systemic shock induced by the effective blockade of this critical maritime chokepoint has precipitated an immediate and violent repricing of global energy assets. Commercial shipping through the region has fallen to near zero as maritime operators weigh the existential risks of missile strikes and drone attacks against their vessels.1 In the absence of viable alternative export routes for key regional producers such as Iraq, Kuwait, and Qatar, global supply chains are experiencing historic levels of stress.5

For Western nations, particularly the United States and European economies, the geopolitical abstraction of a Middle Eastern conflict has rapidly materialized into acute domestic economic pain. The sudden surge in crude oil, natural gas, and refined product prices acts as a massive regressive tax on consumers. This energy shock threatens to reverse years of hard-won disinflationary progress, severely squeeze discretionary household budgets, and derail fragile macroeconomic recoveries.3 The transmission of these elevated global benchmarks to domestic markets is profoundly altering the financial realities of ordinary citizens, manifesting most visibly at the retail fuel pump, but radiating outward into commercial logistics, agricultural production, utility billing, and the cost of everyday consumer goods.

This comprehensive research report provides an exhaustive analysis of the mechanisms through which the 2026 Strait of Hormuz crisis is transmitting inflationary pressures directly to the Western consumer wallet. By evaluating the cascading macroeconomic effects across retail fuel pricing, commercial freight logistics, agricultural spillovers, European utility markets, and broader fiscal policy interventions, this analysis dissects the profound financial implications of the conflict for the average household.

The Geopolitical Catalyst and the Blockade of the Strait of Hormuz

The foundation of the current economic shock lies in the unprecedented disruption of physical energy flows. Following joint United States and Israeli military operations—colloquially termed “Operation Epic Fury”—which aggressively targeted Iranian internal security infrastructure, defense industrial sites, and command capabilities, the Iranian government retaliated by weaponizing its supreme geographic advantage.7 Following the death of Supreme Leader Ayatollah Ali Khamenei on February 28, 2026, his successor, Ayatollah Mojtaba Khamenei, swiftly indicated that the Strait of Hormuz would remain closed to provide strategic leverage for Iran during the ongoing conflict.3

Tehran officially declared that the vital waterway would be closed to vessels originating from the United States, Israel, and their Western allies, while selectively permitting transit for nations exhibiting favorable diplomatic stances, such as China, India, and Turkey.1 The operational realities of the global maritime shipping industry dictate that such declarations, especially when backed by tangible kinetic attacks on commercial vessels, effectively shut down the corridor entirely. The timeline of the escalation illustrates the rapid deterioration of maritime security: on March 1, the oil tanker Skylight was struck by a projectile north of Khasab, Oman, resulting in the deaths of two Indian crew members; by March 4, the Islamic Revolutionary Guard Corps (IRGC) claimed complete control of the strait; and by March 10, a bulk carrier reported a nearby splash and explosion just 36 nautical miles off the coast of Abu Dhabi.1

Consequently, major global shipping firms and insurance underwriters immediately suspended operations. By early March, shipping insurance rates for vessels attempting to navigate the Strait were reported to have surged by four to six times over the previous week’s rates.1 Recognizing the severe threat to global commerce, the United States government invoked the Terrorism Risk Insurance Act to offer federal backing to commercial insurers, while simultaneously demanding that allied nations contribute naval warships to a multinational coalition designed to escort commercial tankers safely through the hazard zone.1 However, the international response has been notably muted; key allies such as Japan and Australia declined to commit naval assets to the region, preferring to lean on diplomatic resolutions and the utilization of strategic reserves.13

The strategic impossibility of completely bypassing the Strait of Hormuz exacerbates the crisis. While Saudi Arabia possesses the East-West Pipeline, which allows millions of barrels of crude to bypass the Persian Gulf and travel to the Red Sea port of Yanbu, this infrastructure cannot fully replace the export volumes normally shipped through the Strait.5 Other major Gulf producers, including Iraq, Kuwait, and Qatar, lack similar pipeline alternatives and were immediately forced to reduce total oil production by at least 10 million barrels per day as local storage facilities rapidly filled to capacity.5 The International Energy Agency (IEA) has characterized this event as the largest disruption to the global energy supply since the 1970s energy crisis, decisively eclipsing the market shocks witnessed during the 2022 Russian invasion of Ukraine.1 Furthermore, the conflict’s collateral damage has expanded beyond the Strait itself; drone attacks on the major oil terminal in Fujairah, United Arab Emirates, temporarily halted vital oil loading operations at a hub located entirely outside of the Hormuz chokepoint.4

The Unprecedented Oil Shock and Global Market Repricing

The sudden and absolute removal of up to 10 million barrels per day of actual production from the global market sent benchmark crude prices soaring, triggering a rapid and violent repricing of global energy assets.14 West Texas Intermediate (WTI) and Brent crude futures experienced extreme volatility as traders and algorithms scrambled to price in a “geopolitical risk premium” that had been largely dormant.

In the immediate aftermath of the Strait’s closure, Brent crude, the international benchmark, spiked from a pre-conflict baseline of approximately $70 per barrel to an intra-day peak of nearly $126 per barrel, representing a staggering increase that rattled global financial markets and stoked fears of a severe global recession.1 Similarly, WTI crude, the United States benchmark, soared to a peak of $119.48 per barrel.10

| Global Energy Benchmark | Pre-Conflict Baseline (Jan/Feb 2026) | Crisis Peak (Early March 2026) | Current Stabilized Volatility Range |

| Brent Crude (Global) | ~$70.00 / barrel | $119.50 – $126.00 / barrel | $92.00 – $104.98 / barrel |

| West Texas Intermediate (US) | ~$63.00 – $70.00 / barrel | $111.00 – $119.48 / barrel | $90.00 – $99.25 / barrel |

| Dutch TTF (European Gas) | €31.00 / MWh | €50.00+ / MWh | €45.00 – €50.00 / MWh |

Data compiled from global commodities trading desks, the International Energy Agency, and regional market reporting.1

While prices subsequently retreated to a highly volatile trading range between $90 and $104 per barrel—driven occasionally by unconfirmed reports of “spy-to-spy” diplomatic backchannels and the announcement of massive coordinated strategic reserve releases—the underlying structural deficit remains unresolved.8 The physical reality of the market is that oil supply chains are facing historic stress. The cost of shipping 2 million barrels of crude oil from the U.S. Gulf Coast to Asia reached a record $29 million, meaning that freight alone now costs $14.50 per barrel, accounting for nearly twenty percent of the total commodity price.18

To place this disruption in historical context, the Arab Oil Embargo of the 1970s removed approximately 4 million barrels per day from the global oil market, equating to roughly seven percent of total consumption at that time.19 The current effective closure of the Strait of Hormuz has the potential to remove some 20 million barrels per day, representing a staggering twenty percent of modern global petroleum liquids consumption.19 Global macroeconomic output simply cannot sustain growth without this vital fifth of its energy supply.5

The inability of producers outside the Middle East to immediately offset this massive supply gap underscores the severe inelasticity of short-term global oil production. While the United States continues to produce at near-record levels—expected to average 13.6 million barrels per day in 2026 and rising to 13.8 million barrels per day in 2027—the structural limitations of drilling, completing, and transporting new domestic shale oil mean that American producers cannot rapidly fill a 20-million-barrel void.20 Even under the most optimistic scenarios assuming $100 a barrel oil, the U.S. Lower 48 could only potentially add another 600,000 barrels per day of production by the fourth quarter of 2026.21 Consequently, the global market is forced into a state of “demand destruction,” an incredibly painful macroeconomic process wherein prices rise so high that consumers and businesses are simply forced to stop consuming energy.

Direct Consumer Impact: The Pain at the United States Fuel Pump

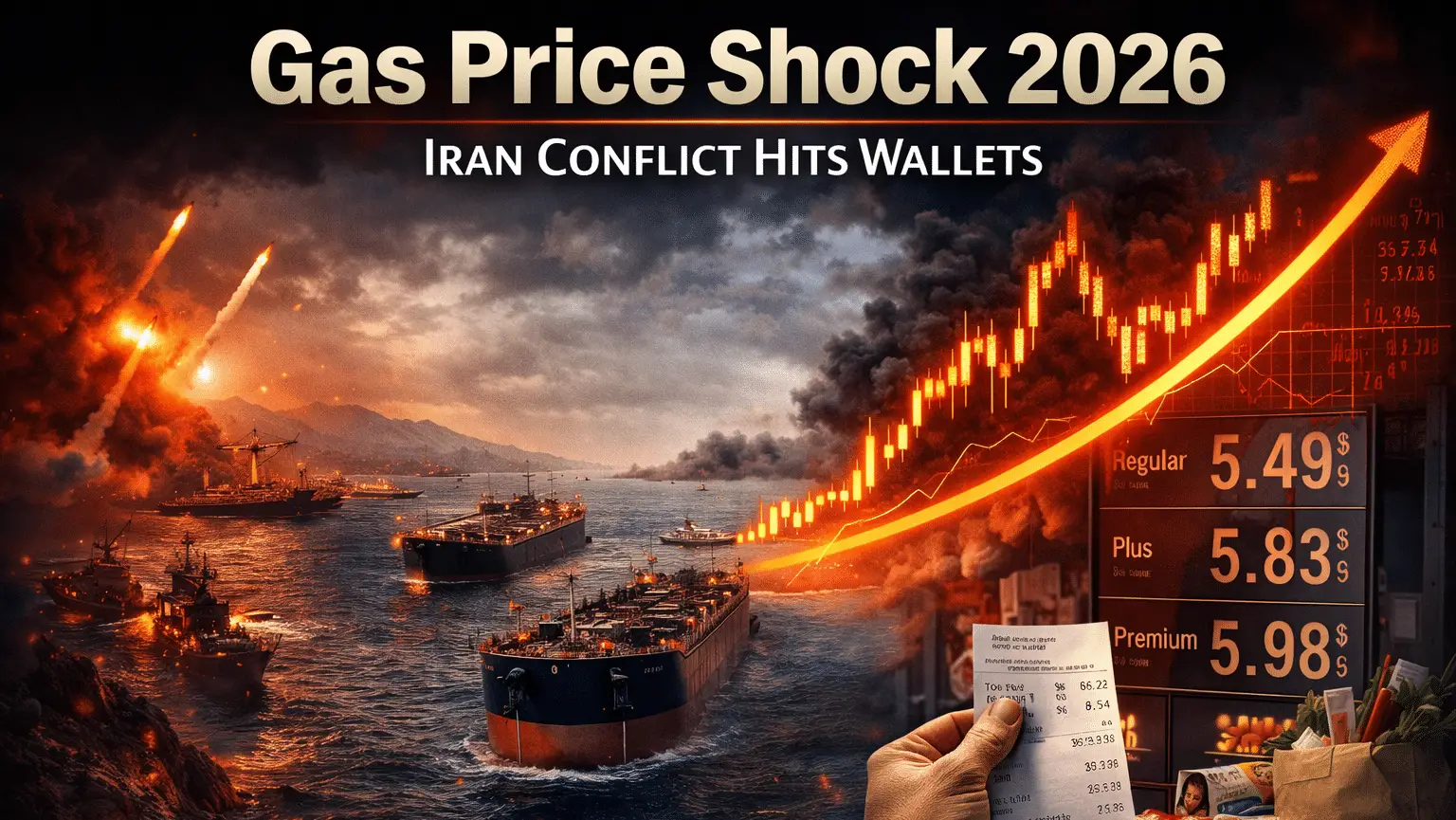

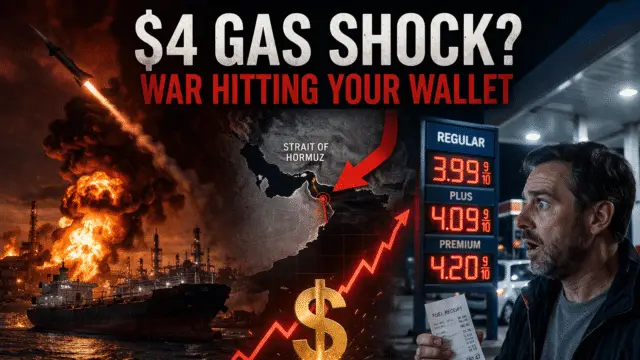

The transmission mechanism from global crude oil benchmarks to the consumer wallet is highly efficient and remarkably rapid. Because crude oil costs account for approximately half of the retail price of gasoline and diesel, a forty to fifty percent surge in global oil markets inevitably leads to a pronounced and immediate shock at the retail fuel pump.3 For the American consumer, the geopolitical abstraction of a distant war translates directly into a degradation of daily purchasing power.

Prior to the outbreak of hostilities, the average American household was benefiting from relatively stable and cooling energy prices. In late February 2026, the national average for a gallon of regular unleaded gasoline stood comfortably at $2.94 to $2.98.3 Within days of the military escalation and the subsequent maritime blockade, the national average surged by more than twenty percent, reaching $3.58 to $3.64 per gallon by mid-March.3 This dramatic reversal entirely wiped out the progress that had been made over the preceding year in lowering pump prices, representing the largest one-day price increases since the market volatility of March 2022.3

However, national averages frequently mask severe regional disparities driven by domestic refining capacity, variable state tax structures, and reliance on imported energy. States possessing robust local oil production and integrated refining infrastructure, such as Louisiana and Texas, experienced more insulated price increases, averaging around $3.20 per gallon.3 In stark contrast, markets heavily dependent on imported refined products—most notably the West Coast—bore the brunt of the crisis. Due to recent refinery closures and a heavy reliance on Asian imports to meet domestic demand, California drivers witnessed average prices skyrocket to $5.34 per gallon, inflicting severe localized economic pain.3 In the Midwest, Michigan motorists saw prices jump to an average of $3.59 per gallon, with consumers paying an average of $54 for a standard 15-gallon fill-up.22

| United States Metric | Pre-War Baseline (Late Feb 2026) | Post-Shock Level (Mid-March 2026) | Percentage Increase |

| National Average Gasoline | $2.94 – $2.98 / gallon | $3.58 – $3.64 / gallon | ~21.7% |

| California Average Gasoline | ~$4.50 / gallon | $5.34 / gallon | ~18.6% |

| Louisiana Average Gasoline | ~$2.80 / gallon | $3.20 / gallon | ~14.2% |

| National Average Diesel | $3.71 / gallon | $4.60 – $4.83 / gallon | ~26.4% |

Data reflects retail pump prices compiled from AAA, the Energy Information Administration, and GasBuddy market analysis.3

The macroeconomic reality of this price appreciation is highly regressive, functioning as a universal tax that disproportionately harms the working class. Data indicates that the bottom sixty percent of U.S. income earners devote nearly four percent of their total take-home pay strictly to gasoline, compared to just two percent for the highest decile of earners.6 This disparity risks further exacerbating the “K-shaped” economic divergence that has characterized the post-pandemic era. For the average American household, which consumes hundreds of gallons of gasoline annually, an extra $10 to $15 per week at the pump immediately forces low-income shoppers to cut discretionary spending in order to afford basic commuting costs.3

Furthermore, the conflict is having a significant impact on global refined product markets. Gulf producers exported roughly 3.3 million barrels per day of refined products in 2025; however, more than 3 million barrels per day of refining capacity in the region has already shut down due to infrastructure attacks and a lack of viable export outlets.14 This bottleneck severely limits the availability of gasoline globally, guaranteeing that upward price pressure will persist at the pump even if crude oil production in non-OPEC nations slightly increases.

The Logistics Meltdown, Freight Surcharges, and the Trucking Industry

While the immediate shock of retail gasoline prices captures the majority of consumer and media attention, the secondary effects transmitted through the commercial transportation sector represent a far more insidious and systemic threat to household budgets. The modern consumer economy is deeply reliant on diesel fuel, which powers the overwhelming majority of heavy-duty freight trucks, national rail networks, maritime cargo vessels, and agricultural machinery.26

The spot market for diesel fuel has exhibited even greater upward volatility than consumer gasoline. Within the first two weeks of the conflict, the national average price for a gallon of diesel in the United States surged by nearly $1.00, climbing 28 percent to reach $4.83, with some regions pushing dangerously close to the all-time historic high of $5.82 recorded in June 2022 following the Russian invasion of Ukraine.3 GasBuddy analysts have projected an 85 percent probability of diesel hitting or exceeding $5.00 a gallon nationally if the geopolitical standoff persists.8

This represents a catastrophic disruption for the United States trucking industry, which was only just beginning to emerge from a grueling, three-year freight recession characterized by excess capacity and depressed spot rates.27 The sudden, violent spike in operating costs has fundamentally altered the mathematical viability of commercial transport, particularly for the small carriers and independent owner-operators that form the backbone of American logistics.

To understand how diesel prices inevitably impact retail goods, one must examine the precise mechanics of freight fuel surcharges. Large, capitalized logistics companies—such as JB Hunt and Schneider National—operate under long-term corporate contracts that include automated, systematic fuel surcharge mechanisms.26 These surcharges are typically tied to the weekly average diesel price published every Monday by the Department of Energy (DOE).8 The industry standard algorithm generally adds one cent per mile to the freight rate for every six-cent increase in the national average diesel price above a predetermined baseline (often set between $1.00 and $1.50 per gallon).8 Consequently, major carriers seamlessly pass the inflated energy costs directly down the supply chain. For example, major rail and intermodal carriers like Union Pacific immediately enacted a staggering 32.0 percent intermodal fuel surcharge for the month of March 2026.28

However, small fleets (those operating between one and twenty trucks) and independent owner-operators operate primarily on the spot market and lack the hedging mechanisms, bulk purchasing agreements, and algorithmic protections of corporate fleets.8 The operating math for these drivers is punishing. A standard Class 8 heavy-duty truck operating at an average fuel efficiency of 6.5 miles per gallon incurs a baseline fuel cost of $0.79 per mile when diesel is $4.60.8 If diesel rises to $5.00 per gallon, this cost instantly jumps to $0.85 per mile. For a standard 2,500-mile cross-country round trip, this creates over $150 in entirely unplanned, unrecoverable fuel expenses per truck, per cycle.8

Without the market leverage to immediately force updated fuel surcharges onto spot market brokers, many independent truckers are forced to operate at a net loss.26 The macroeconomic consequence is highly predictable: as small carriers literally park their trucks and exit the market rather than run unprofitable miles, freight capacity artificially tightens.26 The resulting capacity shortage allows the remaining large carriers to drastically increase base freight rates. Ultimately, these elevated transportation costs are absorbed by wholesale distributors, passed to big-box retailers, and finally levied against the consumer at the checkout counter, driving up the cost of virtually every physical good in the economy.8

Cascading Inflationary Pressures on the Western Wallet

The combination of higher mandatory commuter costs and rapidly inflating freight logistics creates a potent, multi-tiered inflationary cocktail. Prior to the February 2026 escalation, United States inflation was already exhibiting signs of stubborn persistence. In February 2026, the headline Consumer Price Index (CPI) stood at 2.4 percent year-over-year, while core inflation (excluding volatile food and energy sectors) hovered at 2.5 percent—both metrics remaining stubbornly above the Federal Reserve’s stated 2.0 percent target.3 The current oil shock threatens to completely undo recent monetary policy successes and plunge the economy back into an inflationary spiral.

Macroeconomic modeling from major financial institutions indicates that a persistent $100 per barrel oil scenario will drive headline inflation meaningfully higher. Analysts at RBC Capital Markets project that U.S. inflation could breach 3.5 percent by the second quarter of 2026, remaining at that elevated level throughout the calendar year and adding at least 0.7 percentage points to baseline economic forecasts.6 The International Monetary Fund (IMF) has corroborated these severe concerns on a global scale, calculating that every ten percent persistent increase in oil prices pushes global inflation up by 0.4 percentage points while simultaneously reducing worldwide economic output by 0.2 percent.3

The Delayed Shock to the Grocery Aisle

While gasoline prices rise immediately at the pump, the transmission of energy costs to retail food prices operates with a standard lag of 60 to 90 days.26 The agricultural sector is intensely and intrinsically energy-dependent. Modern farming relies heavily on diesel fuel to power tractors, harvesters, combines, and irrigation systems.26 Furthermore, a massive portion of the world’s fertilizer exports—including up to thirty percent of the global supply of urea, ammonia, phosphates, and sulfur—originates from the Middle East and typically transits the Strait of Hormuz.2

As the naval blockade severely restricts the supply of these critical agricultural inputs, global fertilizer prices rise exponentially, vastly increasing the cost of raw crop production. When these higher agricultural production costs are compounded by the aforementioned commercial freight surcharges required to transport food from the farm to the processing plant, and finally to the supermarket, retail food inflation becomes mathematically inevitable. Consumers can expect the price of highly perishable goods, which require rapid, refrigerated, and energy-intensive transportation, to experience the steepest price increases throughout the spring and summer of 2026.3

Plunging Consumer Sentiment and Discretionary Spending Cuts

Faced with mandatory increases in commuting, utility, and nutritional costs, the average consumer will be forced into demand destruction elsewhere in their budget. Monthly surveys of U.S. consumers reveal that households are most likely to aggressively pull back on “food away from home” (restaurant dining)—with 39 percent of respondents indicating immediate cutbacks—followed closely by travel, hospitality, and apparel purchases.31 This sudden reduction in discretionary spending poses a severe risk to the broader service sector, which relies entirely on robust consumer confidence for growth.

The psychological toll of this geopolitical instability and energy anxiety is highly measurable. In March 2026, the University of Michigan Consumer Sentiment Index dropped sharply to 55.5, down from 56.6 the previous month, marking a multi-month low.32 Respondents across all income brackets, age groups, and political affiliations reported significantly weaker expectations for their personal finances moving forward.33

Financial institutions warn of a secondary macroeconomic phenomenon known as the “wealth effect.” If the energy shock triggers a sustained sell-off in global equity markets, the destruction of household wealth invested in 401(k) retirement accounts and stock portfolios could severely depress consumer demand.35 An equity market contraction, combined with higher prices at the checkout counter, accelerates the onset of a broader economic slowdown or a mild recession, paralyzing the economy through both supply constraints and demand destruction.35

The Transatlantic Divide: European Natural Gas and Utility Bills

While the global oil market commands primary attention, the closure of the Strait of Hormuz equally disrupts the flow of liquefied natural gas (LNG), creating a distinct and severe crisis for the European continent. Approximately twenty percent of total global LNG trade passes through this narrow maritime corridor, with massive volumes sourced directly from Qatar and the United Arab Emirates.3

The United States, operating as the world’s leading producer and a net exporter of natural gas, is somewhat structurally insulated from the direct pricing impacts of global LNG shortages. Domestic natural gas prices in the U.S., benchmarked at the Henry Hub, are expected to remain relatively stable, averaging approximately $3.80 per million British thermal units (MMBtu) in 2026.20 This stability is primarily due to existing domestic export constraints that effectively trap excess supply within North America.20 Consequently, the average American household will experience a much more muted impact on their home heating and electricity bills compared to the extreme volatility witnessed at the fuel pump. (Though it should be noted that average retail electricity rates in the U.S. still rose by more than 5 percent over the last year to an average bill of $148.80, driven by grid upgrades and data center power demands 38).

The European Energy Security Crisis Renewed

For Europe, however, the LNG disruption represents a critical and immediate vulnerability. Having painstakingly pivoted away from Russian pipeline gas following the 2022 invasion of Ukraine, Europe grew highly dependent on seaborne LNG imports to sustain its industrial base and heat its homes. Nations like Italy and Belgium source substantial percentages of their total LNG imports—36 percent and 24 percent respectively—directly from Qatar.17

The escalation of the Middle East conflict sent the Dutch TTF—Europe’s primary benchmark for natural gas—surging by roughly 60 percent, leaping from a pre-conflict norm of roughly €31/MWh to over €50/MWh.17 Because natural gas frequently sets the marginal clearing price for electricity in European wholesale markets, the cost of gas-fired power generation doubled in just the first ten days of the conflict.41

This spike in wholesale electricity costs is already devastating European households and heavy industries. The independent think tank Ember calculated that the surge in fossil fuel prices added twice as much to electricity costs as the cost of carbon emissions under the EU Emissions Trading Scheme (ETS).41 In total, the European Union paid an estimated additional €2.5 billion for fossil fuel imports in the first ten days of the crisis alone.17

The crisis has exposed the deep divide in grid resilience across the continent. Nations that have aggressively deployed renewable energy infrastructure, such as Spain, demonstrated significant insulation from the shock; gas influenced the price of electricity in Spain for only 15 percent of hours in early 2026, keeping domestic power prices well below the gas-fired threshold.17 In sharp contrast, heavily gas-reliant grids in Italy (where gas influenced power prices 89 percent of the time) and Germany face renewed challenges regarding industrial competitiveness and widespread household energy poverty.17

United Kingdom Fuel Volatility

In the United Kingdom, the retail fuel market mirrors the extreme volatility seen in the United States. Pump prices rapidly reversed weeks of stability to hit 18-month highs. By early March 2026, the average price of unleaded petrol climbed to approximately 138.2p to 140.6p per litre, while diesel reached 148p to 159.18p per litre.42 Analysts at the Energy and Climate Intelligence Unit estimate that a sustained $100 per barrel crude environment will cost the average British driver (driving 8,000 miles a year) an additional £140 annually, while EU drivers face an average penalty of €220.45 This financial pain will be compounded for UK drivers later in the year, as the government is scheduled to roll back a temporary 5p fuel duty cut introduced during the 2022 crisis, incrementally raising the duty rate beginning in September 2026.46

Government Interventions, Strategic Reserves, and Policy Responses

Faced with a rapidly deteriorating global economic outlook and the severe political liability of surging consumer costs, Western governments have deployed an array of strategic, monetary, and fiscal interventions in desperate attempts to mitigate the crisis and stabilize panicked markets.

The Historic Strategic Petroleum Reserve Release

The most prominent immediate response was coordinated international action executed through the International Energy Agency (IEA). On March 11, 2026, the 32 member nations of the IEA unanimously announced the largest emergency oil release in the organization’s history, authorizing the deployment of 400 million barrels of crude oil and refined products into the global market.3

The United States led this monumental effort, with the Trump administration pledging the release of 172 million barrels—representing 43 percent of the total release—from the U.S. Strategic Petroleum Reserve (SPR) over a 120-day delivery schedule.47 European allies contributed proportionally, with Germany pledging 19.5 million barrels and France contributing 14.5 million barrels.3

While historic in scale—representing more than double the 182.7 million barrels released during the 2022 Ukraine crisis—energy market analysts broadly view the SPR deployment as a temporary analgesic rather than a structural cure.3 The mathematics of the release indicate a supply injection of approximately 3.3 million barrels per day across all participating nations.51 Given that the Strait of Hormuz blockade effectively restricts up to 20 million barrels per day, the SPR release only partially bridges the massive physical supply deficit.

Furthermore, strategic reserves represent a finite inventory. They provide critical short-term liquidity to prevent panic-driven, parabolic price spikes, but they cannot sustainably balance a global market suffering from long-term infrastructure outages.3 The political friction surrounding the SPR is also notable; the current administration has pledged to not only deplete the reserve to manage the crisis but to repurchase and replace approximately 200 million barrels within the next year, creating future obligations that may ultimately support higher baseline oil prices down the road.47

U.S. Domestic Fiscal Policy and the Neutralization of the “One Big Beautiful Bill Act”

Domestically, the United States government has previously attempted to shield consumers and stimulate the working class through aggressive fiscal policy. The “One Big Beautiful Bill Act” (OBBBA), formally signed into law as Public Law 119-21 in July 2025, served as the legislative cornerstone of this economic strategy.52 Designed to put direct cash back into the pockets of the working class and seniors, the OBBBA included several highly publicized and targeted tax deductions set to take effect for the 2026 tax year.

The legislation established the widely discussed “No Tax on Tips” and “No Tax on Overtime” provisions. Under these rules, qualifying individuals are permitted to deduct up to $25,000 in tipped income and $12,500 in mandatory overtime compensation, respectively, provided their modified adjusted gross income falls below $150,000 for single filers.54 Furthermore, the OBBBA expanded the Child Tax Credit from $2,000 to $2,200 per child, increased the standard deduction, introduced a new $10,000 deduction for car loan interest, and provided an additional $6,000 standard deduction for seniors.53

A novel feature of the bill was the creation of “Trump Accounts”—tax-advantaged savings accounts for children under 18, seeded with a one-time $1,000 contribution from the federal government and allowing up to $5,000 in annual private contributions.52 (To finance these expansive tax cuts, the bill raised the national debt ceiling by $5 trillion, implemented a 12 percent cut to Medicaid, and severely limited the tax benefit for charitable contributions to 35 percent of the amount contributed for itemizers 53).

While these extensive tax breaks were explicitly intended to stimulate consumer spending capacity and provide relief from general affordability concerns, current macroeconomic analysis suggests that the 2026 energy shock has effectively neutralized their intended benefits. The sudden transfer of wealth from American households directly to the fuel pump—totaling between $50 billion and $150 billion in nominal consumer spending hits—threatens to entirely absorb the tax savings generated by the OBBBA.6

The lowest-income quintiles, who stand to gain the least from non-refundable tax deductions but spend the highest proportion of their total income on fuel and basic groceries, remain severely exposed.6 In essence, the financial relief promised by the federal government through the tax code is being systematically eroded by the geopolitical realities of the global oil market, leaving the average consumer with little net gain in actual purchasing power.

The Accelerated Transition: Electric Vehicles and Renewable Resilience

Historically, severe energy crises serve as powerful catalysts for structural shifts in consumer behavior and industrial policy. Just as the 1970s oil shocks birthed modern vehicle fuel efficiency standards, the 2026 crisis is noticeably accelerating consumer interest in transportation electrification and broader clean energy investments.

As retail gasoline prices breached the $3.50 to $4.00 per gallon threshold in the U.S., online consumer search volumes for hybrid and fully electric vehicles (EVs) spiked dramatically.57 For the individual consumer, EVs represent a tangible hedge against geopolitical volatility. While electricity prices are indeed subject to general inflation, residential utility rates are heavily regulated by state public utility commissions and change slowly over months or years, effectively insulating EV owners from the violent, daily price shocks witnessed at the retail gasoline pump.58

The mathematical advantage of electric vehicles has widened considerably during the conflict. In the United Kingdom, for example, charging an EV at home on typical off-peak electricity tariffs costs approximately 2p to 7p per mile; in stark contrast, an internal combustion engine vehicle operating at 45 miles per gallon now costs upward of 13p to 14p per mile due to heavily inflated retail fuel costs.59 Analysts at the Energy and Climate Intelligence Unit project that sustained $100 per barrel oil could save European EV drivers approximately €40 million a day collectively, drastically improving the total cost of ownership equation for electric mobility.45

Furthermore, the crisis has highlighted the strategic necessity of transitioning away from fossil fuels to achieve true energy independence. Broad clean energy investments hit a record $2.2 trillion globally in 2025, and the current shock is expected to drive further capital into solar, wind, and grid storage infrastructure, as nations recognize that homegrown renewable energy cannot be blockaded or weaponized by foreign adversaries.60

However, energy economists and supply chain experts caution that while EVs provide localized relief to individual consumer wallets, they do not offer immediate macroeconomic salvation from global oil shocks. The global economy’s deep reliance on hydrocarbons extends far beyond passenger transportation. Crude oil and natural gas are foundational feedstocks to the petrochemical industry, strictly required for the manufacture of plastics, synthetic rubber, asphalt, and fertilizers.25 In nations like China, oil consumption continues to increase despite a massive proliferation of EVs, simply to fuel the country’s growing industrial and petrochemical sectors.57 Furthermore, transitioning a nation’s entire vehicle fleet is a decadal infrastructure process; a sudden surge in EV interest in March 2026 will not alter the aggregate fuel demand profile quickly enough to mitigate the current, acute inflationary crisis.

Conclusion: The Enduring Geopolitical Risk Premium

The 2026 Strait of Hormuz crisis vividly demonstrates the enduring fragility of a highly optimized, fossil-fuel-dependent global economy. The functional closure of the world’s most critical maritime chokepoint has catalyzed a historic energy shock that transcends borders, infiltrating the deepest layers of the Western consumer economy and upending macroeconomic stability.

The immediate takeaway for the average consumer is the unavoidable reality of reduced household purchasing power. The transmission of crude oil spikes to the retail gasoline pump is virtually instantaneous, functioning as a highly visible, regressive tax that immediately degrades household balance sheets and consumer sentiment. More concerning is the secondary wave of inflation currently gathering momentum within the commercial logistics sector. The explosion in diesel prices has fractured the operational economics of the domestic trucking industry, guaranteeing that elevated freight surcharges will soon manifest as higher price tags on retail goods, groceries, and essential services in the months to come.

While aggressive policy interventions, such as the historic 400-million-barrel strategic reserve release, provide necessary psychological stabilization to panicked trading floors and prevent parabolic price extremes, they cannot substitute for physical infrastructure or resolve the underlying geopolitical conflict. Domestic fiscal policies, including the broad tax deductions nested within the One Big Beautiful Bill Act, will undoubtedly offer a degree of financial buffering for certain demographic segments; yet, they are mathematically insufficient to entirely offset the sweeping macroeconomic drag of a sustained $100+ per barrel oil environment.

Looking forward, the persistence of this inflationary shock depends entirely upon the duration of the military conflict and the subsequent reopening of the Strait of Hormuz. Should the crisis extend beyond a few months, central banks—including the Federal Reserve and the European Central Bank—will be forced to navigate a highly precarious stagflationary environment. Policymakers will face the unenviable task of battling supply-driven inflation fueled by unyielding energy costs, while simultaneously managing a consumer base whose discretionary spending is rapidly collapsing under the weight of those exact same costs.

Ultimately, the 2026 crisis underscores a permanent repricing of geopolitical risk in global energy markets. For the Western consumer, the era of frictionless, low-cost energy supply chains may be definitively ending, necessitating a prolonged period of budgetary adaptation and highlighting the urgent economic imperative to accelerate the transition toward domestic, electrified, and geopolitically insulated energy systems.

Leave a Reply